There are several rebalancing strategies that you can utilise to

create an optimal investment process.

| We often discuss the importance of making strategic investment choices, having an asset allocation strategy and putting a financial plan in place for the future, yet we seldom talk about an important part of managing our investment portfolio – rebalancing. |

| If you have an investment portfolio, each security within your portfolio would provide a different return over the course of three months, six months or the year, resulting in a weighting change of your portfolio.1 Portfolio rebalancing is like a periodic tune-up for your portfolio: it helps you keep your risk levels in check as well as minimise risks.1 |

| Simply explained, rebalancing is the process of buying and selling portions of your portfolio in order to set the weight of each asset class back to its original state.1 |

| Why Rebalance Your Portfolio? |

| Periodic rebalancing of your investment portfolio is a good way to keep your investing strategy on track and ensure that your portfolio is not becoming too risky when the market surges or too conservative after major market setbacks.2 Rebalancing is also useful when your personal situation changes – for example, as you move through different life stages, or perhaps when you start a family – as this may change your long-term goals, risk tolerance and asset allocation strategy.3 |

| It is inevitable that over a period of time, differing returns from various asset classes within your portfolio will change the percentages that you have allocated to your original asset mix.1 This change may increase or decrease the risk of your portfolio.1 |

| To understand how rebalancing works, let’s look at a case study comparing a rebalanced portfolio versus one which hasn’t been rebalanced, and the potential results of neglected allocations in a portfolio. |

| A Rebalancing Case Study | ||||

| Lee has RM100,000 to invest. He decides to invest 50% in a bond fund, 10% in a Treasury fund and 40% in an equity fund. | ||||

|

||||

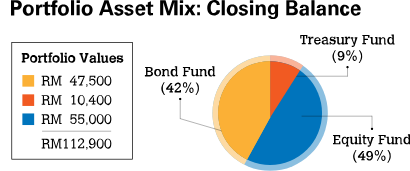

| At the end of the year, Lee’s equity fund portion of his portfolio has dramatically outperformed the other two asset classes. As a result, the percentages of his asset mix have changed considerably. | ||||

|

||||

| As the chart above shows, Lee’s RM40,000 investment in the equity fund has grown to RM55,000 – an increase of 37%. Meanwhile, the bond fund has registered a loss of 5% and the Treasury fund realised a modest increase of 4%. | ||||

| The overall return on Lee’s portfolio was 12.9%, but now, there’s more weight on equities than on bonds. Lee might be willing to leave the asset mix as it is for the time being, but leaving it for too long could result in an overweighting in the equity fund, which is riskier than the bond and Treasury funds. | ||||

| A popular belief among many investors is that if an investment has performed well over the last year, it should perform well over the next year. As a result, many investors like Lee may remain heavily invested in last year’s “winning” equity fund and drop his portfolio weighting in last year’s “losing”fixed income fund. | ||||

| So let’s compare the values of Lee’s rebalanced portfolio versus if he had left it unchanged the following year. | ||||

|

||||

|

||||

| At the end of the second year, the equity fund performs poorly and loses 7%. At the same time, the bond fund performs well and gains 15%,while Treasuries remain relatively stable with a 2% increase. If Lee had rebalanced his portfolio after the first year, his total portfolio value would be RM118,500 – an increase of 5%. | ||||

|

||||

| But if Lee had left his portfolio unchanged, his total portfolio value would be RM116,858 – a gain of only 3.5%. In this case, rebalancing would have been the optimal strategy. | ||||

| It could have been possible that if the stock markets had rallied again through the second year, Lee’s equity fund would have appreciated more, and the unchanged portfolio may have realised a greater gain in value. But at what risk? Just as with many hedging strategies, the upside potential may be limited, but by rebalancing, you are adhering to your risk-return tolerance level.1 | ||||

| Remember: the goal of rebalancing is not about boosting your long-term returns.2 Rather, the aim of rebalancing is to manage risk.2 It is a way to keep your portfolio’s asset mix in sync with your risk tolerance level.2 | ||||

| Basic Steps for Rebalancing Your Portfolio | ||||

|

||||

|

Rebalancing Strategies

Calendar Rebalancing

Calendar rebalancing is the most basic rebalancing approach.4 This strategy simply involves analysing your investment holdings within your portfolio at predetermined time intervals and adjusting to the original asset allocation at a desired frequency.4 Monthly and quarterly assessments are typically preferred because weekly rebalancing would be too costly while a yearly approach would allow for too much intermediate portfolio drift.4 The ideal frequency of rebalancing should be determined based on time constraints, transaction costs and allowable drift.4

The advantage of calendar rebalancing over formulaic rebalancing is that it is less time consuming, since formulaic rebalancing requires continuous attention.4

Percentage of Portfolio Rebalancing

A preferred but slightly more intensive approach involves a rebalancing schedule based on the allowable percentage composition of an asset in your portfolio.4 Each asset class is given a target weight and a corresponding tolerance range.4

For example, your allocation strategy may include the requirement to hold 30% in emerging market equities, 30% in domestic blue chips and 40% in government bonds with a tolerance of +/-5% for each asset class.4 When the weight of any one asset class drifts outside the allowable band – in this case 25% to 35% for emerging market and blue chip equities and 35% to 45% for government bonds – the entire portfolio is rebalanced to reflect the initial target composition.4

Constant Proportion Portfolio Insurance

This third rebalancing approach strategy assumes that as your wealth increases as an investor, so does your risk tolerance.4 The basic premise of this strategy stems from having a preference of maintaining a minimum safety reserve held in either cash or risk-free government bonds.4 When the value of the portfolio increases, more funds are invested in equities, while a fall in portfolio value results in a smaller position towards risky assets.4 This strategy of rebalancing is useful when you need to maintain a safety reserve – whether it will be used to fund your child’s educational expenses or be put towards the purchase of a home.4

Whichever strategy you choose, portfolio rebalancing ultimately provides protection and discipline for your chosen investment strategy.4 The ideal strategy will balance out the overall needs of rebalancing with the costs associated with the strategy chosen.4

Absolute Amount

Apart from rebalancing your existing portfolio, you can also increase the overall portfolio size by topping up your portfolio value. It’s worth noting that if you are adding new money to your portfolio, in some cases it might be more beneficial to simply not contribute any new funds to the asset class that is overweighted while continuing to contribute to other asset classes that are underweighted. Your portfolio might be able to rebalance over time without you incurring capital gains taxes.3

Mistakes to Avoid When Rebalancing Your Portfolio

|

||

|

||

|

Losing Focus

You won’t rebalance effectively if you don’t know what’s going on. HSBC’s Wealth Dashboard, for example, allows you to log on and monitor your investment portfolio day-by-day. It’s less about finding the most optimal time to rebalance and more about finding a system that works for you as an investor so you can stick with it. Consistency matters more than the actual day or month. |

Speak to your Relationship Manager or walk into any

HSBC branch for your portfolio review and rebalancing.

HSBC branch for your portfolio review and rebalancing.

• Sources: 1 Investopedia, Rebalance Your Portfolio to Stay on Track, 30 January 2018. 2 CNN Money, Is it Really Necessary to Rebalance Your Investment Portfolio? 24 January 2018. 3 Wealth Advocates, Portfolio Rebalancing in Today’s Market, 20 December 2017. 4 Investopedia, Types of Rebalancing Strategies, 30 January 2018.